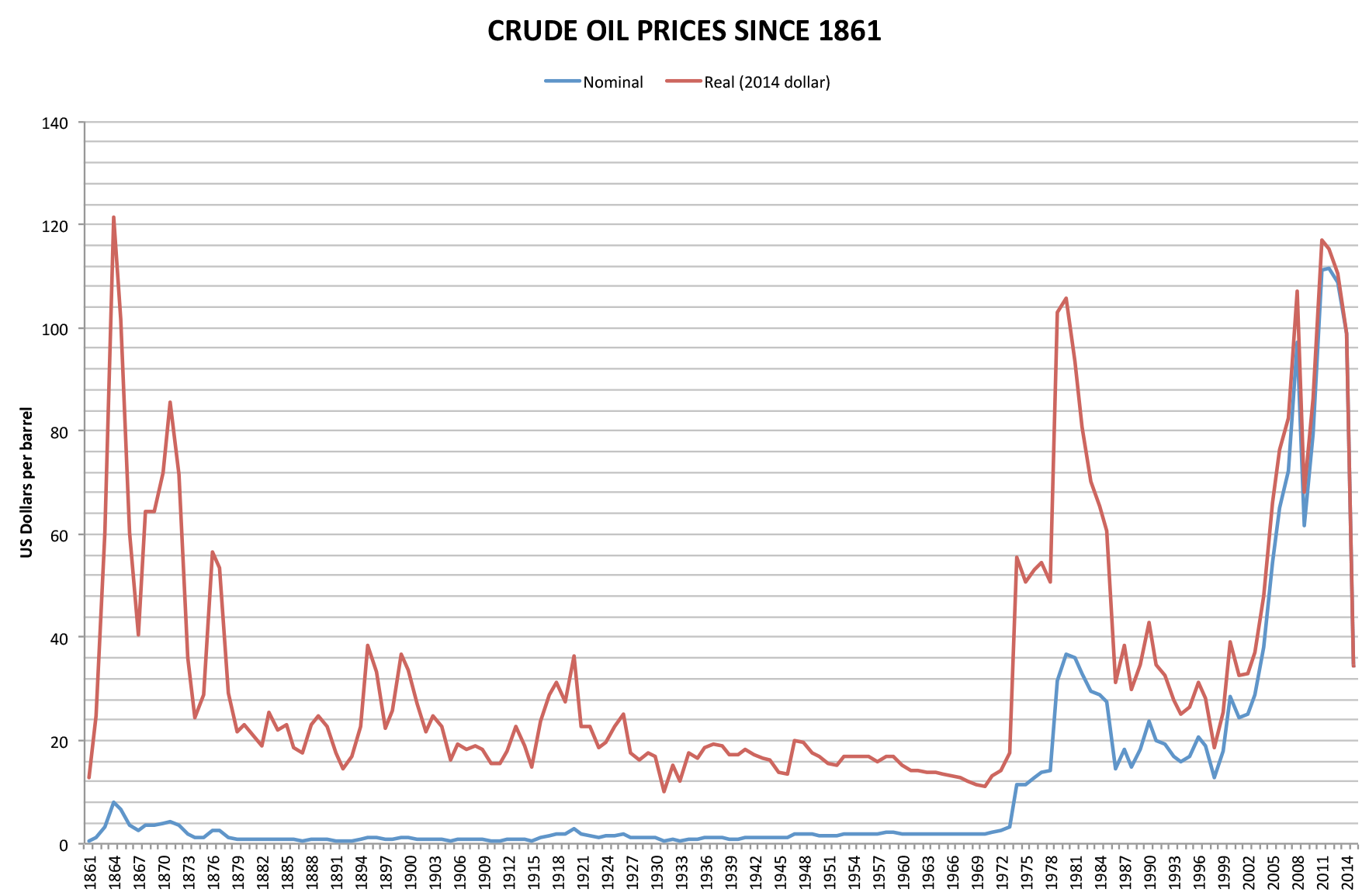

Iran war stock market impact is easiest to understand when you treat markets as a pricing engine for energy risk, policy response, and earnings durability, not a simple referendum on whether conflict headlines are positive or negative. Use this page with Will Iran War Raise Gas Prices?, Strait of Hormuz Closure Timeline, and Strait of Hormuz War Risk Insurance to connect market moves with the shipping and commodity channels that usually move first.

Investor confusion usually comes from mixing time horizons. Day-one price action reflects uncertainty, options hedging, and liquidity gaps; week-two performance reflects revised crude assumptions, inflation expectations, and whether policymakers signal containment. The most reliable process is to track cross-asset confirmation: crude futures, breakeven inflation, Treasury yields, and credit spreads should be interpreted as one system rather than separate headlines.

How does Iran war affect stock market pricing mechanically?

Start with transmission channels. A Middle East escalation adds a geopolitical premium to crude, which feeds directly into expected fuel, transport, and input costs. That pushes inflation expectations higher at the margin, and even a modest shift can reprice rate-sensitive equities when valuations are already elevated. In parallel, investors raise required returns for risk assets, which compresses multiples in sectors where cash flows are longer-duration and most dependent on stable financing conditions.

The second mechanical channel is positioning. Funds that entered the quarter with high equity beta or crowded growth exposure may de-risk quickly, creating sharp intraday drawdowns that look larger than fundamental changes would justify. But once liquidity stabilizes and scenario probabilities tighten, the same positioning pressure can reverse, producing fast rallies. This is why the first move after conflict escalation is often directionally useful but rarely complete: a market shock is a repricing sequence, not a single print.

| Channel | Fast Signal | Equity Effect | What Confirms It |

|---|---|---|---|

| Energy shock | Brent/WTI spike | Margin pressure in fuel users | Sustained move over 3-5 sessions |

| Inflation repricing | Higher breakevens | Multiple compression in long-duration growth | Parallel move in real yields |

| Risk premium | Wider credit spreads | Index-level volatility and lower breadth | Persistent spread widening |

Why oil prices and Treasury yields drive the first equity reaction

Investors asking how does iran war affect stock market behavior should watch the crude-yield pair before anything else. Oil shocks are immediate and visible, while earnings revisions arrive later. If crude jumps but Treasury yields fall, markets may be pricing growth damage with eventual policy support. If crude and yields rise together, investors are pricing a stagflation-style mix that tends to pressure broad indexes and particularly expensive sectors. The distinction is critical for allocating risk within days instead of reacting after consensus catches up.

Duration matters. A one-week dislocation can be absorbed if shipping lanes stay open and emergency inventories normalize flows. A multi-week disruption, especially through key maritime corridors, increases odds of sustained inflation pressure and weaker discretionary demand. That is why market desks cross-check conflict reports with physical flow data, insurance costs, and freight signals rather than relying on political statements alone. Oil direction without context can be misleading; oil persistence is what changes portfolio math.

In this cycle, crude persistence mattered more than crude peaks for equity drawdown depth.

Which sectors usually underperform when middle east risk premiums jump?

Airlines, logistics-heavy retailers, and other fuel-intensive businesses often absorb the first earnings risk when energy costs move faster than pricing power. Transportation contracts can lag spot fuel changes, and many firms cannot fully pass through cost shocks without demand destruction. Consumer discretionary names with thin margins and high financing needs can face a double hit: weaker disposable income from higher gasoline costs plus tighter financial conditions if yields remain elevated.

Financials are more nuanced than many headlines suggest. Large institutions may benefit from trading volumes during volatility, but credit-sensitive lenders can face deterioration if households and small businesses absorb a prolonged energy-tax effect. Semiconductor and software names with strong balance sheets can hold up better than expected if investors view conflict risk as temporary and AI or productivity narratives remain intact. Sector outcomes depend less on labels and more on cash-flow resilience, debt structure, and pricing leverage.

| Sector | Main Vulnerability | What Improves Outlook | What Worsens Outlook |

|---|---|---|---|

| Airlines | Jet fuel and route disruption | Fast crude reversal | Extended corridor instability |

| Consumer discretionary | Fuel-driven household squeeze | Wage resilience | Higher financing costs |

| Transport/logistics | Freight and insurance repricing | Stable transit security | War-risk premium persistence |

Which sectors can outperform during iran conflict volatility?

Energy producers are the obvious relative winners when crude rises, but quality within the group matters. Upstream firms with disciplined capex, strong free-cash-flow conversion, and manageable leverage generally outperform highly indebted producers in volatile windows. Integrated majors can gain from diversified earnings streams when refining and trading offset some upstream variability. The core risk for late buyers is mean reversion: conflict premiums can unwind faster than many portfolios can rebalance.

Defense and aerospace often attract flows when security spending expectations rise, but valuation discipline is essential because consensus can crowd quickly. Some infrastructure, cybersecurity, and mission-critical industrial names can also benefit if governments and enterprises accelerate resilience spending. That said, dispersion inside each "beneficiary" bucket is wide. Investors who rely on theme labels without balance-sheet and valuation checks often underperform despite correctly calling the macro direction.

The better framing is scenario-adjusted expectancy. Ask what price already assumes about duration, what earnings revisions are plausible, and what downside exists if diplomacy de-escalates faster than expected. A good trade in a bad entry zone becomes a poor portfolio decision.

Why stocks can rally even while war headlines get worse

Markets price change, not absolute fear. If participants expected a full shipping shutdown but observed partial continuity, equities can rise even with ongoing strikes because reality is "less bad" than the prior distribution. This dynamic explains why many investors feel disconnected from tape action during geopolitics. The narrative sounds worse while probabilities quietly improve under the surface.

Three forces usually drive that relief pattern: policy signaling that major powers want containment, evidence that physical flows remain functional, and corporate guidance that avoids broad demand collapse language. When these conditions hold, index breadth can widen and volatility compress even before media narratives catch up. You can see this relationship in synchronized declines in oil volatility, high-yield spreads, and the VIX term-structure kink.

How to compare iran war oil prices and stocks without overfitting

Overfitting happens when analysts force every index move into a single-cause story. To avoid that trap, split your framework into baseline and shock layers. Baseline includes earnings trend, valuation regime, and policy path that existed before escalation. Shock layer includes crude path, shipping disruption, and conflict duration assumptions. When you isolate layers, you can estimate how much of the move is geopolitical versus cyclical or structural.

Use fixed observation windows: 1 day, 5 days, 20 days. In each window, compare S&P sector relative performance against crude change and yield change. If correlation flips between windows, avoid high-conviction narrative calls until stabilization appears. This method reduces emotional trading because you are evaluating pattern quality, not headline intensity. It also prevents repeatedly "discovering" relationships that only existed for one volatile session.

What a practical 30-day scenario framework looks like

A useful scenario matrix has only three branches: containment, rolling disruption, and severe expansion. In containment, maritime interruptions remain limited and crude drifts lower; equity leadership broadens beyond energy and defense. In rolling disruption, transit uncertainty and insurance costs stay elevated; sector dispersion remains wide and index upside is capped by inflation sensitivity. In severe expansion, physical supply risk rises materially; inflation and growth fears can hit equities and bonds simultaneously.

Assign explicit probabilities and review cadence. For example, reassess every 72 hours unless a major shipping or policy event forces an immediate update. Tie each branch to portfolio actions: hedge ratio, cash buffer, and position limits for high-beta sectors. The value of the framework is not perfect prediction; it is disciplined adaptation. Teams that pre-commit decision rules usually make fewer late-cycle emotional moves.

| Scenario | Primary Signal | Likely Equity Pattern | Risk Action |

|---|---|---|---|

| Containment | Lower crude volatility | Breadth expansion, defensives lag | Reduce tactical hedges gradually |

| Rolling disruption | High shipping premium | Sector rotation, choppy indexes | Keep barbell exposure |

| Severe expansion | Sustained flow loss | Broad de-risk, higher correlation | Raise cash and index protection |

How portfolio risk controls should change during geopolitical shocks

Risk control is about process speed and position sizing, not heroic prediction. First, reduce concentration in names where liquidity can gap lower in stress windows. Second, predefine invalidation levels for every tactical position so exits are mechanical when scenarios break. Third, avoid layering leverage on assumptions that depend on one political headline. Geopolitical tapes can reverse faster than execution quality allows.

For long-only portfolios, temporary hedges can reduce forced-selling risk and buy decision time. For active portfolios, pair trades can isolate thesis exposure while minimizing macro beta drift. Most importantly, document why each position exists under each scenario branch. If you cannot state the "why" in one sentence tied to observable indicators, position size is probably too large for the current uncertainty regime.

This discipline aligns with broader conflict risk context in Iran Missile Attack Risk Index and strategic framing in US vs Iran. Portfolio resilience improves when market and security analysis use the same probability logic.

What to monitor daily to see if market risk is easing or compounding

Build a compact dashboard with ten fields: Brent level, Brent volatility, 2-year Treasury yield, 10-year breakeven inflation, dollar index trend, high-yield spread, VIX front-month, airline and transport relative strength, defense/energy breadth, and verified maritime disruption updates. The point is not complexity; it is consistency. When most fields improve together, risk is easing. When crude, volatility, and spreads worsen together, treat rallies as tactical until confirmation improves.

Source quality matters as much as indicator selection. For macro baselines use the IMF World Economic Outlook; for energy flow context use the U.S. Energy Information Administration petroleum reports; and for high-frequency conflict updates cross-check with Reuters Middle East coverage. Mixing high-quality primary sources with a stable indicator set reduces false alarms.

| Indicator Group | Easing Signal | Stress Signal | Update Cadence |

|---|---|---|---|

| Energy + shipping | Lower premiums, calmer transit | Rising insurance and reroutes | Daily |

| Rates + inflation | Stable real yields | Higher breakevens with weak breadth | Daily |

| Credit + volatility | Tighter spreads, lower VIX | Spread widening with index weakness | Intraday + close |

Bottom line: how to read iran war stock market impact with discipline

Use a three-layer rule: first read energy and shipping stress, second read rates and inflation expectations, third read sector breadth and credit confirmation. If those layers point in the same direction, market signal quality is high. If they diverge, reduce conviction and position size until the picture clarifies. This approach keeps you from chasing fear spikes or fading legitimate stress too early.

Most investors do not lose money from missing the first move; they lose from forcing certainty during uncertainty. A structured dashboard, explicit scenario probabilities, and predefined risk actions are the practical edge in this cycle. The objective is not to predict every headline, but to stay aligned with how markets actually reprice geopolitical risk through oil, rates, earnings, and confidence.

FAQ: Iran war stock market impact

How does Iran war affect stock market performance?

The fastest transmission channel is oil, which changes inflation and rate expectations in days, not quarters. Equity indexes can fall or rally depending on whether investors price a brief disruption or a prolonged supply shock.

Which sectors benefit from Iran war volatility?

Energy producers and some defense names often gain relative strength when crude prices rise and governments increase security spending. Sector leadership still depends on duration, earnings quality, and valuation at entry.

Should investors buy oil stocks during Iran conflict headlines?

Buying only on headlines can backfire if risk premium fades quickly after diplomacy signals. A better process is to size positions around scenario probabilities and pre-defined exit rules.

Why can stocks rise during a war shock?

Markets are forward-looking, so indexes can rise when investors believe the conflict will stay geographically contained and temporary. Falling oil and stabilizing bond yields usually confirm that risk pricing is normalizing.

What indicators signal Iran war market risk is easing?

Watch for lower crude volatility, tighter credit spreads, and a decline in implied volatility alongside calmer shipping and insurance updates. Broad confirmation across assets matters more than one rally day in equities.

Related analysis: Will Iran War Raise Gas Prices?, Strait of Hormuz Closure Timeline, Iran Missile Attack Risk Index, and US vs Iran.